RST sells computer equipment and prepares its financial statements to 31 December.

On 30 September 20X5 RST sold computer software along with a two year maintenance package to a customer. The customer is given the right to return the goods within six months and claim a full refund if they are not satisfied with the computer software. The risk of return is considered to be insignificant for RST.

How should the revenue from this transaction and the right of return be recognised in the financial statements for the year ended 31 December 20X5?

JJ's current share price is $1.80, with a dividend of $0.20 a share just about to be paid.

Dividends have increased at an average annual growth rate of 4.5% and this is expected to continue into the future.

What is JJ's cost of equity?

GH is a listed entity which holds equity shares in one subsidiary and one associate.

Information extracted from the most recent financial statements is as follows:

What is the interest cover for the year?

XY has a weighted average cost of capital (WACC) of 12%. The debt:equity ratio is 1:3 and this is considered low for the industry. XY needs to raise finance to purchase new machinery in the coming year.

Which of the following forms of finance is most likely to increase the WACC?

Which TWO of the following statements about bonds and their issue are true?

ST acquired 75% of the 2 million $1 equity shares of CD on 1 January 20X3, when the retained earnings of CD were S3,550,000. CD has no other reserves.

ST paid $5,600,000 for the shares in CD and the non controlling interest was measured at its fair value of S1,400,000 at acquisition.

At 1 January 20X3, the fair value of CD's net assets were equal to their carrying amount, with the exception of a building. This building had a fair value of $1,000,000 in excess of its carrying amount and a remaining useful life of 25 years on 1 January 20X3.

At 31 December 20X5, the retained earnings of ST and CD were $8,500,000 and $5,250,000 respectively.

What is the figure for non-controlling interest to be shown in the consolidated statement of financial position of ST as at 31 December 20X5?

On 1 January 20X4 JK had 1,500,000 ordinary shares in issue. On 1 September 20X4 JK issued 600,000 ordinary shares at the market value of $2.50 a share. For the financial year ended 31 December 20X4 the statement of profit or loss shows profit before tax of $625,000 and profit after tax of $500,000.

What is the earnings per share for the year ended 31 December 20X4?

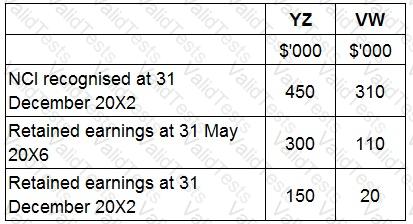

AB acquired 90% of the equity of YZ on 31 December 20X2. On the same date YZ acquired 60% of the equity shares of VW for $750,000. AB has no other subsidiaries.

The following information regarding YZ and VW was available:

What amount will AB include in its consolidated statement of financial position in respect of non controlling interest at 31 May 20X6?

KL acquired 75% of the equity share capital of MN on 1 January 20X8. The group's policy is to value non-controlling interest at fair value at the date of acquisition. MN acquired 60% of the equity share capital of PQ on 1 January 20X9 for $360 million.

At 1 January 20X9 the fair value of the non-controlling interest in PQ was $220 million and the fair value of the net assets of PQ at 1 January 20X9 were $320 million.

Calculate the goodwill arising on the acquisition of PQ at 1 January 20X9.

Give your answer to the nearest million.

$ ? million

The directors of AB want to reduce the entity's gearing ratio in the year to 31 December 20X9.

Which of the following independent actions could the directors take during 20X9 to achieve this?