A bank extends a loan of $1m to a home buyer to buy a house currently worth $1.5m, with the house serving as the collateral. The volatility of returns (assumed normally distributed) on house prices in that neighborhood is assessed at 10% annually. The expected probability of default of the home buyer is 5%.

What is the probability that the bank will recover less than the principal advanced on this loan; assuming the probability of the home buyer's default is independent of the value of the house?

If the returns of an asset display a strong tendency for mean reversion, what is the relationship between annualized volatility calculated based on daily versus weekly volatilities (using the square root of time rule)?

The CDS quote for the bonds of Bank X is 200 bps. Assuming a recovery rate of 40%, calculate the default hazard rate priced in the CDS quote.

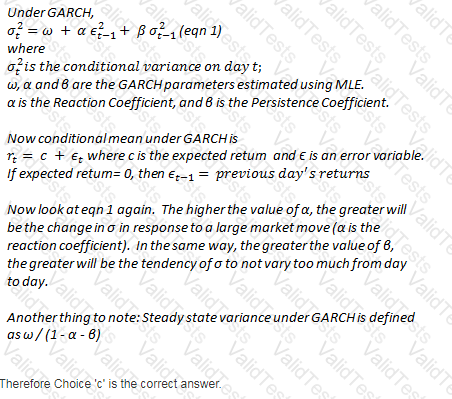

As the persistence parameter under GARCH is lowered, which of the following would be true:

The minimum 'multiplication factor' to be applied to VaR calculations for calculating the capital requirements for the trading book per Basel II is equal to:

Which of the following statements is true

I. If no loss data is available, good quality scenarios can be used to model operational risk

II. Scenario data can be mixed with observed loss data for modeling severity and frequency estimates

III. Severity estimates should not be created by fitting models to scenario generated loss data points alone

IV. Scenario assessments should only be used as modifiers to ILD or ELD severity models.

An investor enters into a 5-year total return swap with Bank A, with the investor paying a fixed rate of 6% annually on a notional value of $100m to the bank and receiving the returns of the S&P500 index with an identical notional value. The swap is reset monthly, ie the payments are exchanged monthly. On Jan 1 of the fourth year, after settling the last month's payments, the bank enters bankruptcy. What is the legal claim that the hedge fund has against the bank in the bankruptcy court?

If the cumulative default probabilities of default for years 1 and 2 for a portfolio of credit risky assets is 5% and 15% respectively, what is the marginal probability of default in year 2 alone?

Who has the ultimate responsibility for the overall stress testing programme of an institution?

Which of the following is closest to the description of a 'risk functional'?